Under-Valued or Over-Valued Property Value Tax-Wise?

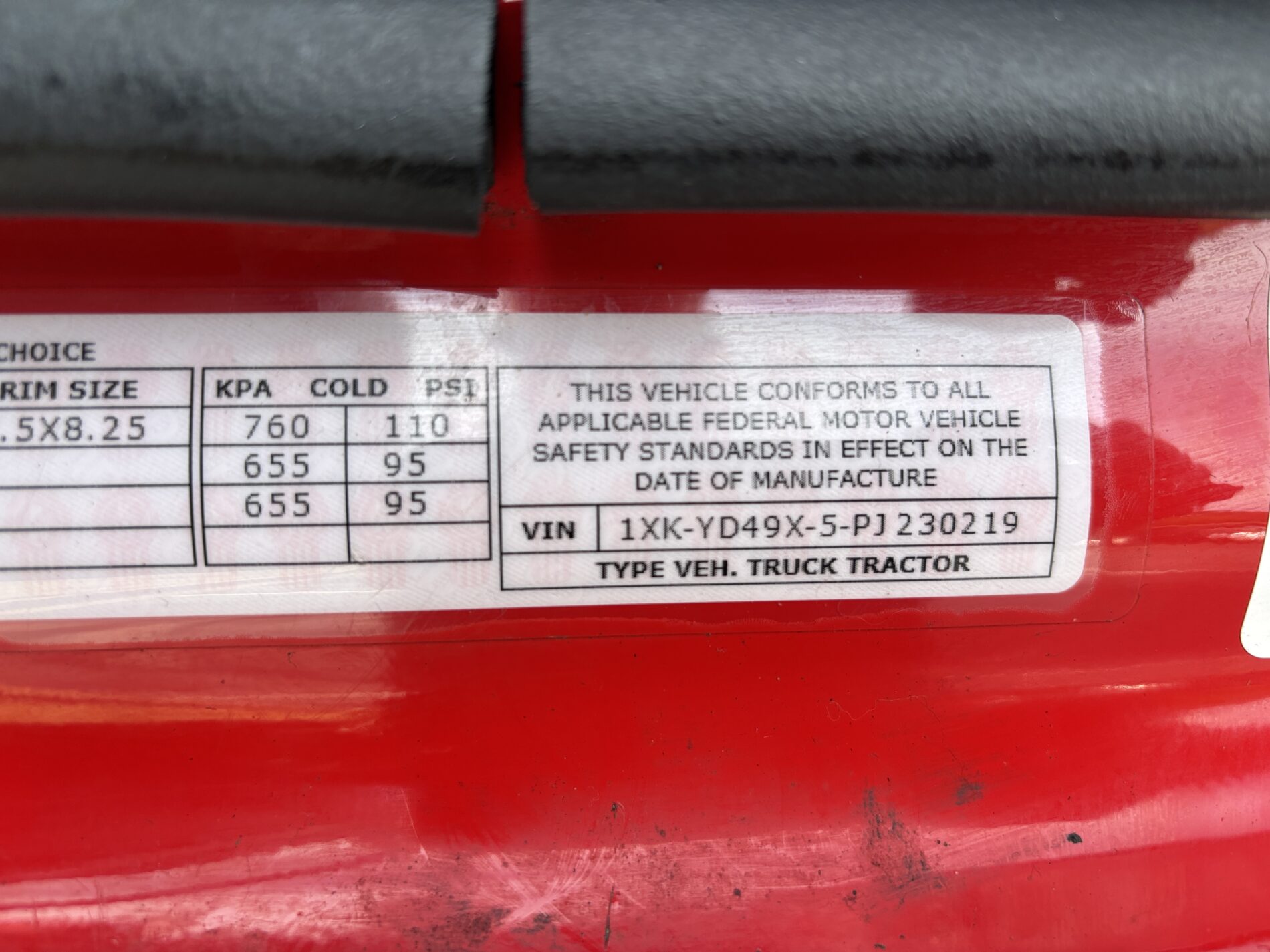

With so many variations in how Class 8 and Class 7 trucks are built, without the VIN and the truck manufacturer’s build sheet, there is no way the vehicle property tax systems in North Carolina or Virginia can properly determine the value of any commercial truck. Either state may be under-valuing or over-valuing your truck(s). The chances are your truck(s) are over-valued.

Who knows, you might be over-taxed by $2,000.00, $5,000 or more per truck. Get your FREE market value analysis to see if you are being overtaxed. Complete the Tax Appraisal Inquiry Form and provide photos of the truck you’re inquiring about.

North Carolina (Retail Value) – Virginia (J.D. Power “Clean Trade-In”)

Virginia First – Short and to the point.

Virginia state law (Virginia Code Section 58.1-3503.A.3) requires the Commissioner of Revenue to assess vehicles using values found in a “recognized pricing guide,” thus ensuring uniformity and equity of all assessments within a jurisdiction. The use of individual vehicle sales or trade-in offers as a basis for assessment is not a valid reason for appeal.

To meet these requirements, Arlington uses one of the lowest January 1 values, the“clean loan value,” in the J.D. Power guide.

North Carolina Department of Revenue (NCDOR) GS105-187.3.(a) Rate of Tax

(a) Tax Base. The tax imposed by this Article is applied to the sum of the retail value of a motor vehicle for which a certificate of title is issued and any fee regulated by G.S. 20-101.1. The tax does not apply to the sales price of a service contract, provided the charge is separately stated on the bill of sale or other similar document given to the purchaser at the time of the sale.

(b) Retail Value. – The retail value of a motor vehicle for which a certificate of title is issued because of a sale of the motor vehicle by a retailer is the sales price of the motor vehicle, including all accessories attached to the vehicle when it is delivered to the purchaser, less the amount of any allowance given by the retailer for a motor vehicle taken in trade as a full or partial payment for the purchased motor vehicle.

The retail value of a motor vehicle for which a certificate of title is issued because of a sale of the motor vehicle by a seller who is not a retailer is the market value of the vehicle, less the amount of any allowance given by the seller for a motor vehicle taken in trade as a full or partial payment for the purchased motor vehicle. A transaction in which two parties exchange motor vehicles is considered a sale regardless of whether either party gives additional consideration as part of the transaction.

The retail value of a motor vehicle for which a certificate of title is issued because of a reason other than the sale of the motor vehicle is the market value of the vehicle. The market value of a vehicle is presumed to be the value of the vehicle set in a schedule of values adopted by the Commissioner.

(c) Schedules. – In adopting a schedule of values for motor vehicles, the Commissioner shall adopt a schedule whose values do not exceed the wholesale values of motor vehicles as published in a recognized automotive reference manual.

So what is the actual value you are being taxed on? Retail Value, Market Value, or Wholesale Value?

Is it the JD Power Commercial Truck values considered as the recognized automotive reference manual for wholesale values?

Just remember this: your truck IS NOT dealer retail-ready! Wholesale value ready, most likely.

Appealing Tax Values North Carolina – Virginia

North Carolina Appeals Process Conflicts with (NCDOR) GS105-187.3.(a)

Registered Motor Vehicles (Wake County Website)

Licensed motor vehicles are valued at retail market value for property tax purposes in accordance with the North Carolina Vehicle Valuation Manual. A motor vehicle offered for sale by a dealer to the end consumer represents the best example of the retail market value.

- Licensed motor vehicles are not valued at wholesale, blue book, trade-in or private party asking price for property tax purposes.

- There are various online valuation tools available. These sites often offer trade-in, wholesale, private-party, and retail market values.

- Trade-in values represent what you might expect a dealer to offer you for your vehicle to apply toward the purchase of another car in the dealer’s inventory.

- Wholesale values represent the value the dealer would pay to purchase a vehicle from a car manufacturer or from a dealer auction.

- Private-party value is the price one could expect for vehicle sales between a private buyer and a private seller.

- Retail market value is the sales price of a vehicle purchased from a dealer, including all accessories attached to the vehicle. This is the value used to reflect retail level of trade for property tax purposes.

Value adjustments may be necessary if the owner can document:

- High mileage

- Significant body or frame damage

- Excessively worn interior

- Other damage that may significantly reduce the retail value

- Note: normal wear and tear will not be considered.

Documentation that will be considered for a vehicle value appeal:

- A copy of the bill of sale documenting the purchase price from a local dealer

- A written appraisal performed by a dealer or qualified appraiser that clearly states the appraisal reflects the retail value as of the January 1 of the year in which the taxes are due

- For vehicles less than eight years old, documentation of high mileage from an annual inspection, oil change or other invoice

- Repair estimates for vehicles that have been significantly damaged

Documentation that will not be considered for a vehicle value appeal:

- Wholesale (black book) or trade-in values pulled from any internet valuation website, magazine or catalog

- A trade-in or wholesale value appraisal from a dealer

- Written offers from a dealer to purchase your vehicle

- A bill of sale from a private seller

Appeal Deadline: Licensed vehicle value appeals and all supporting documentation must be postmarked within 30 days of the due date printed on the notice.

Virginia

To appeal a vehicle’s value, you must have the vehicle valued by an expert appraiser, adjuster, or auto repair facility (e.g., car dealer, insurance appraiser, car auctioneer, or automobile mechanic).

The written appraisal must:

- Be on the appraiser’s letterhead.

- Include the appraiser’s name, address, phone number, and signature.

- Include a description of the vehicle’s condition on January 1 of the assessment’s tax year.

- Include a detailed damage and repair estimate listing the specific conditions that lower the vehicle’s value than the clean trade-in value listed in the J.D Power (formally NADA Guides).

- Examples are excessive rust, body damage, missing engine, etc. Excess mileage alone is not a sufficient reason for a reassessment of your vehicle; however, you can apply for a high mileage adjustment if the vehicle qualifies. For more information, go to the Vehicle High Mileage Appeal tab.